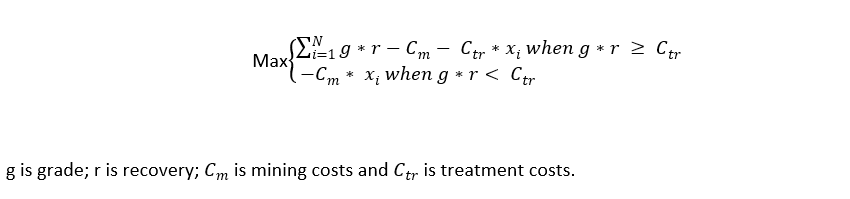

The stochastic approach has played a critical role in optimizing the pit limit. The growing demand for stochastic methods is driven by increasing uncertainty in mining projects. For example, the uncertain true grade in block models necessitates the use of simulations. Recently, not only technical factors but also financial risks—such as commodity prices and costs—have been taken into account. Using the stochastic approach for pit optimization, Dimitrakopoulos and Abdel Sabour (2007) found that it can increase revenue by 11% based on Australian mines. Henry et al. (2005) confirmed the impact of grade and commodity price uncertainty on pit optimization, concluding that the stochastic approach can enhance value by 6% in a small deposit case. Marcotte and Caron (2013) proposed a linear programming model to maximize block profit:

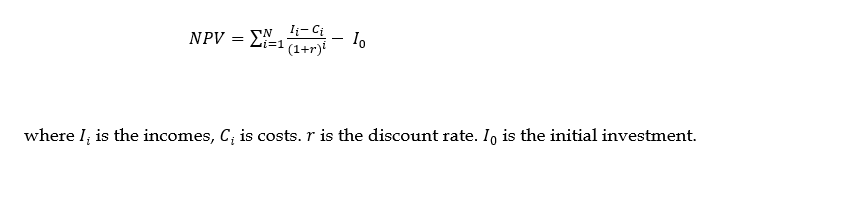

However, they ignored the discount rate, which seems to fail in addressing future uncertainty. Therefore, the recent pit optimization has included the discount rate in calculating the net present value (NPV).

The formula is expressed as follows: